Can You Get Larger Home Loan For Repairs Furniture Va Loan

The VA home loan: Unbeatable benefits for veterans

For many who qualify, the VA loan program is the best possible mortgage.

Backed by the U.Due south. Department of Veterans Affairs, VA loans are designed to help agile-duty military personnel, veterans and sure other groups go homeowners at an affordable cost.

The VA loan asks for no down payment, requires no mortgage insurance, and has lenient rules nearly qualifying, among many other advantages.

Here'south everything y'all need to know about qualifying for and using a VA loan.

In this commodity (Skip to...)

- Summit 10 VA loan benefits

- VA loan rates

- VA loan eligibility

- How to become your COE

- Credit and income to qualify

- Funding fees and loan limits

- Eligible property types

- Veteran mortgage relief

- When Non to use a VA loan

- Spouses and the VA mortgage program

- VA loan assumption

- Utilize for a VA loan

Top 10 VA loan benefits

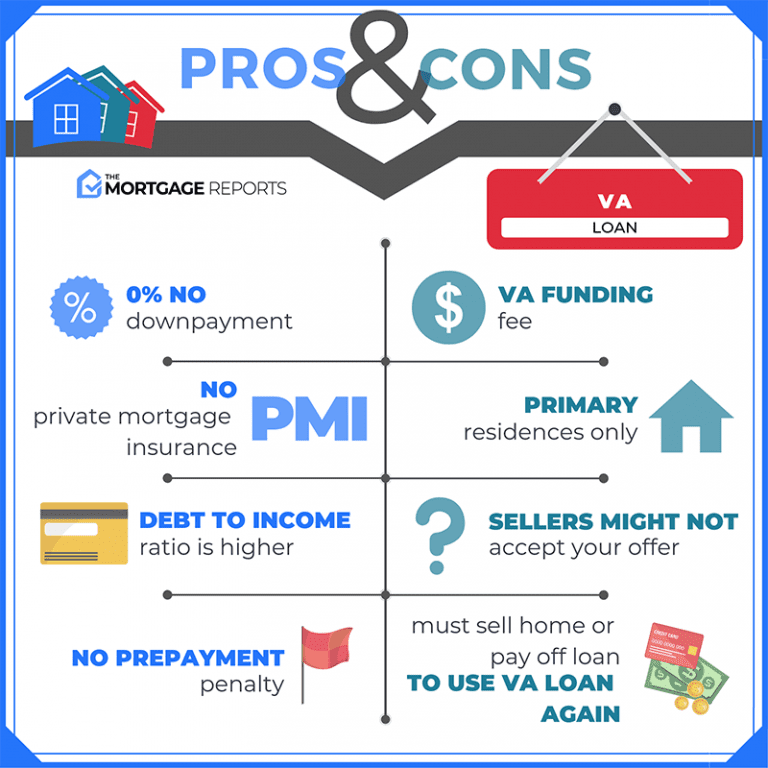

1. No downwardly payment on a VA loan

Nearly dwelling house loan programs require you to make at least a small down payment to purchase a home. The VA home loan is an exception.

Rather than paying 5%, 10%, 20% or more of the home'southward purchase price upfront in cash, with a VA loan you can finance upwards to 100% of the buy price.

The VA loan is a true no-money-downwards home mortgage opportunity.

2. No mortgage insurance for VA loans

Typically, lenders require y'all to pay for mortgage insurance if you lot make a down payment that's less than twenty%.

This insurance — which is known as private mortgage insurance (PMI) for a conventional loan and a mortgage insurance premium (MIP) for an FHA loan — would protect the lender if you defaulted on your loan.

VA loans require neither a down payment nor mortgage insurance. That makes a VA-backed mortgage very affordable upfront and over time.

3. VA loans accept a government guarantee

At that place's a reason why the VA loan comes with such favorable terms.

The federal government guarantees these loans — significant a portion of the loan corporeality will be repaid to the lender even if you're unable to brand monthly payments for whatever reason.

This guarantee encourages and enables private lenders to offer VA loans with exceptionally attractive terms.

iv. You tin shop for the best VA loan rates

VA loans are neither originated nor funded past the VA. They are non directly loans from the government. Furthermore, mortgage rates for VA loans are non set past the VA itself.

Instead, VA loans are offered by U.S. banks, savings-and-loans institutions, credit unions, and mortgage lenders — each of which sets its own VA loan rates and fees.

This means you tin shop around and compare loan offers and notwithstanding choose the VA loan that works best for your upkeep.

five. VA loans don't allow a prepayment penalisation

A VA loan won't restrict your right to sell the property partway through your loan term.

There's no prepayment penalty or early on-exit fee no affair within what time frame you lot determine to sell your home.

Furthermore, in that location are no restrictions regarding a refinance of your VA loan.

You can refinance your existing VA loan into some other VA loan via the agency'south Involvement Charge per unit Reduction Refinance Loan (IRRRL) program, or switch into a non-VA loan at any fourth dimension.

6. VA mortgages come in many varieties

A VA loan can have a fixed rate or an adjustable rate. In add-on, you lot tin use a VA loan to buy a firm, condo, new-built home, manufactured domicile, duplex, or other types of backdrop.

Or, information technology can be used for refinancing your existing mortgage, making repairs or improvements to your home, or making your home more energy-efficient.

The choice is yours. A VA-approved lender can help you decide.

vii. It's easier to authorize for VA loans

Like all mortgage types, VA loans require specific documentation, an acceptable credit history, and sufficient income to make your monthly payments.

But, compared to other loan programs, VA loan guidelines tend to exist more flexible. This is made possible because of the VA loan guarantee.

The Department of Veterans Affairs genuinely wants to make the loan process easier for military machine members, veterans, and qualifying military spouses to buy or refinance a home.

viii. VA loan closing costs are lower

The VA limits the closing costs lenders tin can accuse to VA loan applicants. This is some other way that a VA loan tin can be more than affordable than other types of loans.

Money saved on closing costs tin can be used for furniture, moving costs, home improvements, or annihilation else.

9. The VA offers funding fee flexibility

VA loans require a "funding fee," an upfront cost based on your loan amount, your blazon of eligible service, your downward payment size, and other factors.

Funding fees don't need to exist paid in cash, though. The VA allows the fee to be financed with the loan, so nothing is due at closing.

And, not all VA borrowers will pay it. VA funding fees are usually waived for veterans who receive VA disability compensation and for unmarried surviving spouses of veterans who died in service or as a result of a service-connected disability.

ten. VA loans are assumable

Near VA loans are "assumable," which means y'all can transfer your VA loan to a time to come home heir-apparent if that person is as well VA-eligible.

Assumable loans tin can be a huge benefit when you sell your home — especially in a ascent mortgage rate environment.

If your home loan has today's low rate and market rates ascent in the hereafter, the assumption features of your VA go even more valuable.

VA loan rates

The VA loan is viewed equally one of the lowest-risk mortgage types bachelor on the market place.

This prophylactic allows banks to lend to veteran borrowers at lower interest rates.

Today's VA loan rates*

| Loan Type | Current Mortgage Rate |

| VA xxx-twelvemonth FRM | % (% APR) |

| Conventional 30-twelvemonth FRM | % (% Apr) |

| VA xv-year FRM | % (% Apr) |

| Conventional 15-yr FRM | % (% April) |

*Current rates provided daily by partners of the Mortgage Reports. See our loan assumptions here.

VA rates are more than than 25 ground points (0.25%) lower than conventional rates on boilerplate, according to data collected by mortgage software company Ellie Mae.

Most loan programs require higher downwards payment and credit scores than the VA abode loan. In the open market place, a VA loan should carry a higher rate due to more lenient lending guidelines and higher perceived risk.

Nevertheless the result of the Veterans Diplomacy efforts to keep veterans in their homes means lower risk for banks and lower borrowing costs for eligible veterans.

VA mortgage calculator

Eligibility

Am I eligible for a VA dwelling loan?

Contrary to popular belief, VA loans are bachelor not only to veterans, simply also to other classes of military members.

The list of eligible VA borrowers includes:

- Agile-duty service members

- Members of the National Baby-sit

- Reservists

- Surviving spouses of veterans

- Cadets at the U.Due south. Military, Air Force or Coast Guard Academy

- Midshipmen at the U.S. Naval University

- Officers at the National Oceanic & Atmospheric Administration.

A minimum term of service is typically required.

Minimum service required for a VA mortgage

VA dwelling house loans are available to active-duty service members, veterans (unless dishonorably discharged), and in some cases, surviving family unit members.

To be eligible, you lot need to meet one of these service requirements:

- You've served 181 days of active duty during peacetime

- You lot've served 90 days of agile duty during wartime

- Yous've served six years in the Reserves or National Baby-sit

- Your spouse was killed in the line of duty and you lot have not remarried

Your eligibility for the VA habitation loan program never expires.

Veterans who earned their VA entitlement long ago are yet using their benefit to buy homes.

The VA loan Certificate of Eligibility (COE)

What is a COE?

In order to evidence a mortgage company you are VA-eligible, you'll need a Certificate of Eligibility (COE). Your lender can acquire ane for yous online, usually in a matter of seconds.

How to get your COE (Certificate of Eligibility)

Getting a Certificate of Eligibility (COE) is very piece of cake in most cases. Simply take your lender order the COE through the VA'due south automated system. Whatsoever VA-approved lender can practise this.

Alternatively, yous can order your certificate yourself through the VA benefits portal.

If the online organization is unable to issue your COE, you'll need to provide your DD-214 form to your lender or the VA.

Does a COE mean you are guaranteed a VA loan?

No, having a Certificate of Eligibility (COE) doesn't guarantee a VA loan approving.

Your COE shows the lender you're eligible for a VA loan, but no one is guaranteed VA loan approving.

Y'all must however qualify for the loan based on VA mortgage guidelines. The guarantee part of the VA loan refers to the VA's promise to the lender of repayment if the borrower defaults.

Qualifying for a VA mortgage

VA loan eligibility vs. qualification

Being eligible for VA home loan benefits based on your military status or affiliation doesn't necessarily mean you'll authorize for a VA loan.

You still have to qualify for a VA mortgage based on your credit, debt, and income.

Minimum credit score for a VA loan

The VA has established no minimum credit score for a VA mortgage.

All the same, many VA mortgage lenders require minimum FICO scores of 620 or higher — so use with many lenders if your credit score might be an issue.

Even VA lenders that allow lower credit scores don't accept subprime credit.

VA underwriting guidelines country that applicants must take paid their obligations on fourth dimension for at to the lowest degree the most recent 12 months to exist considered satisfactory credit risks.

In addition, the VA unremarkably requires a two-year waiting period following a Chapter 7 bankruptcy or foreclosure before it volition insure a loan.

Borrowers in Affiliate xiii must have made at to the lowest degree 12 on-time payments and secure the approval of the bankruptcy courtroom.

VA loan debt-to-income ratios

The relationship of your debts and your income is called your debt-to-income ratio, or DTI.

VA underwriters split up your monthly debts (car payments, credit cards, and other accounts, plus your proposed housing expense) past your gross (before-revenue enhancement) income to come up with your debt-to-income ratio.

For instance:

- If your gross income is $4,000 per calendar month

- And your total monthly debt is $1,500 (including the new mortgage, property taxes and homeowners insurance, plus other debt payments)

- And so your DTI is 37.five% (1500/4000=0.375)

A DTI over 41% ways the lender has to utilize additional formulas to see if y'all authorize under residual income guidelines.

VA residual income rules

VA underwriters perform additional calculations that can impact your mortgage approval.

Factoring in your estimated monthly utilities, your estimated taxes on income, and the area of the country in which you alive, the VA arrives at a effigy which represents your "true" costs of living.

It then subtracts that effigy from your income to find your residual income (e.thou. your coin "left over" each month).

Think of the residuum income calculation as a real-world simulation of your living expenses.

It is the VA'due south best effort to ensure that military families have a stress-free homeownership experience.

Here is an example of how residual income works, assuming a family of 4 which is purchasing a ii,000 square-foot home on a $5,000 monthly income.

- Future house payment, plus other debt payments: $2,500

- Monthly estimated income taxes: $1,000

- Monthly estimated utilities at $0.xiv per square foot: $280

This leaves a residual income adding of $i,220.

Now, compare that residue income to for a family of 4:

- Northeast Region: $1,025

- Midwest Region: $1,003

- S Region: $1,003

- West Region: $one,117

The borrower in our example exceeds VA's residual income standards in all parts of the country.

Therefore, despite the borrower'due south debt-to-income ratio of 50%, the borrower could get approved for a VA loan.

Qualifying for a VA loan with part-fourth dimension income

You can qualify for this type of financing even if you lot accept a part-time chore or multiple jobs.

You must evidence a 2-year history of making consistent part-time income, and stability in the number of hours worked. The lender will make sure any income received appears stable. Come across our complete guide to getting a mortgage when you lot're cocky-employed or work part-time.

VA funding fees and loan limits

About the VA funding fee

The VA charges an upfront fee to defray the costs of the plan and brand information technology sustainable for the future.

Veterans pay a lump sum that varies depending on the loan purpose and down payment amount.

The fee is ordinarily wrapped into the loan. It does non add to the cash needed to shut the loan.

VA habitation purchase funding fees

| Type of Military machine Service | Down Payment | Fee for First-Time Employ | Fe e for Subsequent Use |

| Agile Duty, Reserves, and National Guard | None | 2.3% | 3.half dozen% |

| five% or more | ane.65% | 1.65% | |

| ten% or more than | one.4% | ane.iv% |

VA cash-out refinance funding fees

| Type of Military Service | Fee for Offset-Fourth dimension Utilise | Fee for Subsequent Uses |

| Active Duty, Reserves, and National Guard | ii.three% | iii.6% |

VA streamline refinances (IRRRL) & assumptions

| Blazon of Military Service | Fee for Starting time-Time Apply | Fee for Subsequent Uses |

| Agile Duty, Reserves, and National Guard | 0.v% | 0.five% |

Manufactured home loans not permanently affixed

| Type of Military Service | Fee for First-Time Employ | Fee for Subsequent Uses |

| Active Duty, Reserves, and National Baby-sit | 1.0% | i.0% |

VA loan limits in 2022

VA loan limits take been repealed, cheers to the Blueish Water Navy Vietnam Veterans Human action of 2022.

There is no maximum amount for which a home heir-apparent tin receive a VA loan, at to the lowest degree as far as the VA is concerned.

Nevertheless, individual lenders may set their ain limits. So check with your lender if you are looking for a VA loan above local conforming loan limits.

Eligible property types

Houses you can buy with a VA loan

VA mortgages are flexible most what types of holding you can and tin't buy. A VA loan tin can exist used to buy a:

- Discrete business firm

- Condo

- New-built habitation

- Manufactured home

- Duplex, triplex or four-unit property

You can as well utilize a VA mortgage to refinance an existing loan for whatever of those types of backdrop.

VA loans and second homes

Federal regulations limit loans guaranteed by the Section of Veterans Affairs to "primary residences" only.

Withal, "primary residence" is divers as the habitation in which you alive "most of the twelvemonth."

Therefore, if yous own an out-of-state residence in which you alive for more than half dozen months of the twelvemonth, this other home, whether it's your vacation home or retirement holding, becomes your official "primary residence."

For this reason, VA loans are popular among aging military borrowers.

Buying a multi-unit dwelling with a VA loan

VA loans allow you lot to buy a duplex, triplex, or iv-plex with 100% financing. You must alive in i of the units.

Buying a domicile with more than one unit tin be challenging.

Mortgage lenders consider these properties riskier to finance than traditional, single-family unit residences, then you'll need to be a stronger borrower.

VA underwriters must make sure you will accept enough emergency savings, or cash reserves, after closing on your business firm. That's to ensure you lot'll accept money to pay your mortgage even if a tenant fails to pay rent or moves out.

The minimum greenbacks reserves needed subsequently closing is half dozen months of mortgage payments (roofing chief, involvement, taxes, and insurance - PITI).

Your lender will too want to know about previous landlord experience you've had, or any experience with property maintenance or renting.

If you don't have any, you may exist able to sidestep that result by hiring a property management visitor. Just that'due south up to the private lender.

Your lender will expect at the income (or potential income) of the rental units, using either existing rental agreements or an appraiser's opinion of what the units should fetch.

They'll commonly accept 75% of that amount to showtime your mortgage payment when computing your monthly expenses.

VA loans and rental backdrop

Y'all cannot utilize a VA loan to buy a rental property. You lot can, however, use a VA loan to refinance an existing rental domicile you once occupied as a chief home.

For home purchases, in society to obtain a VA loan, you must certify that you intend to occupy the dwelling as your main residence.

If the holding is a duplex, triplex, or 4-unit apartment building, you must occupy ane of the units yourself. Then you can hire out the other units.

The exception to this dominion is the VA'southward Interest Rate Reduction Refinance Loan (IRRRL).

This loan, too known as the VA Streamline Refinance, tin be used for refinancing an existing VA loan on a home where you currently live or where yous used to alive, merely no longer practise.

Ownership a condo with a VA loan

The VA maintains a listing of approved condo projects inside which you may purchase a unit of measurement with a VA loan.

At VA's website, you can search for the thousands of approved condominium complexes beyond the U.S.

If you are VA-eligible and in the market for a condo, make certain the unit of measurement you're interested in is approved.

As a heir-apparent, you are probably not able to get the complex VA-approved. That's up to the management visitor or homeowner's association.

If a condo you similar is not canonical, you must use other financing like an FHA or conventional loan or find some other property.

Note that the condo must meet FHA or conventional guidelines if you want to utilise those types of financing.

Veteran mortgage relief with the VA loan

The U.S. Department of Veterans Affairs, or VA, provides dwelling retention assistance. The VA intervenes when a veteran is having trouble making home loan payments.

The VA works with loan servicers to offer loan options to the veteran, other than foreclosure.

In financial year 2022, the VA made over 400,000 contact actions to attain borrowers and loan servicers. The intent was to work out a mutually amusing repayment option for both parties.

More than 100,000 veteran homeowners avoided foreclosure in 2022 lonely thanks to this effort.

The initiative has saved the taxpayer an estimated $ii.6 billion. More importantly, vast numbers of veterans and military families got another chance at homeownership.

When NOT to use a VA loan

If you have good credit and 20% down

A main reward to VA home loans is the lack of mortgage insurance.

However, the VA guarantee does not come complimentary of charge. Borrowers pay an upfront funding fee, which they usually choose to add together to their loan amount.

The fee ranges from 1.4% to 3.half-dozen%, depending on the downward payment percent and whether the dwelling buyer has previously used his or her VA mortgage eligibility. The most common fee is 2.iii%.

On a $200,000 purchase, a two.3% fee equals $4,600.

However, buyers who choose a conventional mortgage and put twenty% down become to avoid mortgage insurance and the upfront fee. For these military home buyers, the VA funding fee might be an unnecessary expense.

The exception: Mortgage applicants whose credit rating or income meets VA guidelines just non those of conventional mortgages may withal opt for VA.

If yous're on the "CAIVRS" listing

To authorize for a VA loan, y'all must show you have fabricated good on previous government-backed debts and that you have paid taxes.

The Credit Alert Verification Reporting System, or "CAIVRS," is a database of consumers who take defaulted on government obligations. These individuals are not eligible for the VA home loan programme.

If y'all have a non-veteran co-borrower

Veterans oft apply to buy a home with a non-veteran who is not their spouse.

This is okay. Even so, it might non exist their best choice.

Every bit the veteran, your income must cover your half of the loan payment. The non-veteran's income cannot be used to compensate for the veteran's insufficient income.

Plus, when a not-veteran owns half the loan, the VA guarantees only half that amount. The lender will require a 12.5% down payment for the not-guaranteed portion.

The Conventional 97 mortgage, on the other hand, allows down payments as depression as 3%.

Another low-down-payment mortgage option is the FHA home loan, for which 3.5% downwards is acceptable.

The USDA home loan as well requires zero downwardly payment and offers similar rates to VA loans. Nevertheless, the belongings must exist within USDA-eligible areas.

If y'all plan to borrow with a non-veteran, one of these loan types might exist your better choice.

If y'all apply with a credit-challenged spouse

In states with community property laws, VA lenders must consider the credit rating and financial obligations of your spouse. This rule applies fifty-fifty if he or she volition not exist on the home'due south title or even on the mortgage.

Such states are equally follows.

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

A spouse with less-than-perfect credit or who owes alimony, child support, or other maintenance can brand your VA approving more challenging.

Apply for a conventional loan if you authorize for the mortgage by yourself. The spouse's financial history and status need not be considered if he or she is not on the loan application.

If you want to buy a vacation home or investment property

The purpose of VA financing is to assistance veterans and active-duty service members buy and alive in their own home. This loan is non meant to build real estate portfolios.

These loans are for principal residences simply, then if you want a ski cabin or rental, you lot'll take to go a conventional loan.

If y'all want to purchase a high-end home

Starting January 2022, there are no limits to the size of mortgage a lender tin can approve.

However, lenders may establish their own limits for VA loans, and then check with your lender before applying for a large VA loan.

Spouses and the VA mortgage program

What spouses are eligible for a VA loan?

What if the service member passes away earlier he or she uses the benefit? Eligibility passes to an unremarried spouse, in many cases.

For the surviving spouse to be eligible, the deceased service member must take:

- Died in the line of duty

- Passed abroad as a effect of a service-connected disability

- Been missing in action, or a prisoner of war, for at least 90 days

- Been a totally disabled veteran for at least 10 years prior to decease, and died from any cause

Too eligible are remarried spouses who married after the age of 57, on or after December 16, 2003.

In these cases, the surviving spouse tin utilize VA loan eligibility to buy a dwelling with nix down payment, just as the veteran would have.

VA loan benefits for surviving spouses

Surviving spouses have an additional VA loan benefit, however. They are exempt from the VA funding fee. As a result, their loan balance and monthly payment will be lower.

Surviving spouses are besides eligible for a VA streamline refinance when they meet the following guidelines.

- The surviving spouse was married to the veteran at the time of death

- The surviving spouse was on the original VA loan

VA streamline refinancing is typically not available when the deceased veteran was the only applicant on the original VA loan, even if he or she got married after buying the home.

In this example, the surviving spouse would demand to qualify for a non-VA refinance, or a VA greenbacks-out loan.

A cash-out mortgage through VA requires the military spouse to see home purchase eligibility requirements.

If this is the case, the surviving spouse can tap into the habitation's equity to raise greenbacks for whatsoever purpose, or even pay off an FHA or conventional loan to eliminate mortgage insurance.

Qualifying if you receive (or pay) child support or alimony

Ownership a home after a divorce is no easy chore.

If, prior to your divorce, you lived in a 2-income household, you now have less spending power and a reduced monthly income for purposes of your VA dwelling house loan awarding.

With less income, it can exist harder to run into both the VA Home Loan Guaranty's debt-to-income (DTI) guidelines and the VA residual income requirement for your area.

Receiving alimony or child back up tin counteract a loss of income.

Mortgage lenders will non require y'all to provide data about your divorce agreement'southward alimony or child back up terms, just if you're willing to disembalm, information technology tin can count toward qualifying for a home loan.

Different VA-approved lenders will treat pension and child support income differently.

Typically, you lot will be asked to provide a copy of your divorce settlement or other courtroom paperwork to support the alimony and child support payments.

Lenders will then want to see that the payments are stable, reliable, and likely to continue for another 36 months, at to the lowest degree.

You may likewise exist asked to show proof that alimony and child support payments have been fabricated in the past reliably, so that the lender may utilize the income as function of your VA loan application.

If you are the payor of alimony and child support payments, your debt-to-income ratio can exist harmed.

Non but might you be losing the 2d income of your dual-income households, but you're making additional payments that count confronting your outflows.

VA mortgage lenders brand careful calculations with respect to such payments.

You can still go approved for a VA loan while making such payments — it's just more than difficult to evidence sufficient monthly income.

VA loan assumption

What is VA loan assumption?

I benefit for home buyers is that VA loans are assumable. When you assume a mortgage loan, yous take over the current homeowner'due south monthly payment.

That could be a big advantage if mortgage rates have risen since the original possessor purchased the dwelling. The heir-apparent would exist able to acquire a depression-charge per unit, affordable loan — and it could make it easier for the seller to discover a willing buyer in a tough market.

VA loan supposition savings

Ownership a home via an assumable mortgage loan is even more than appealing when interest rates are on the rise.

For case:

- Say a seller-financed $200,000 for their abode in 2022 at an interest rate of 3.25% on a thirty-year stock-still loan

- Using this scenario, their primary and interest payment would exist $898 per month

- Let's assume current thirty-twelvemonth fixed rates averaged four.ten%

- If yous financed $200,000 at iv.x% for a 30-twelvemonth loan term, your monthly chief and involvement payment would be $966 per month

Additionally, because the seller has already paid four years into the loan term, they've already paid most $25,000 in interest on the loan.

By assuming the loan, you lot would save $34,560 over the thirty-twelvemonth loan due to the difference in interest rates. You lot would also relieve roughly $25,000 thanks to the interest already paid by the sellers.

That comes out to a total savings of most $60,000!

How to assume (take on) a VA loan

There are currently two ways to assume a VA loan.

- The new buyer is a qualified veteran who "substitutes" his or her VA eligibility for the eligibility of the seller

- The new domicile heir-apparent qualifies through VA standards for the mortgage payment. This is the safest method for the seller every bit information technology allows the loan to be causeless knowing that the new buyer is responsible for the loan, and the seller is no longer responsible for the loan

The lender and/or the VA needs to approve a loan assumption.

Loans serviced by a lender with automatic authorisation may process assumptions without sending them to a VA Regional Loan Center.

For lenders without automatic authority, the loan must be sent to the appropriate VA Regional Loan Center for blessing. This loan procedure will typically take several weeks.

When VA loans are assumed, it's the servicer's responsibility to make certain the homeowner who assumes the property meets both VA and lender requirements.

VA loan assumption requirements

For a VA mortgage assumption to take place, the following weather must be met:

- The existing loan must be current. If non, any past due amounts must be paid at or earlier closing

- The heir-apparent must qualify based on VA credit and income standards

- The buyer must assume all mortgage obligations, including repayment to the VA if the loan goes into default

- The original owner or new owner must pay a funding fee of 0.5% of the existing principal loan residual

- A processing fee must exist paid in accelerate, including a reasonable estimate for the cost of the credit report

Finding assumable VA loans

There are several ways for home buyers to find an assumable VA loan.

Believe information technology or not, print media is still live and well. Some domicile sellers advertise their assumable home for sale in the paper, or in a local real estate publication.

There are a number of online resources for finding assumable mortgage loans.

Websites like TakeList.com and Zumption.com give homeowners a fashion to showcase their backdrop to home buyers looking to assume a loan.

With the help of the Multiple Listing Service (MLS), existent estate agents remain a great resource for home buyers.

This applies to home buyers specifically searching for assumable VA loans as well.

How do I employ for a VA loan?

Yous can easily and speedily have a lender pull your document of eligibility (COE) to make certain y'all're able to get a VA loan.

Most mortgage lenders offer VA home loans. So you're complimentary to shop and compare rates with merely virtually any visitor that catches your eye.

Getting a VA loan for your new home is similar in many ways to securing any other buy loan. In one case you discover an platonic home in your price range, you brand a purchase offering, and and so undergo VA appraisal and underwriting.

VA appraisal ensures that the home meets its minimum holding requirements (MPRs) and is structurally audio and safe for occupancy.

What's more, VA-specific mortgage lenders are really some of the highest-rated (and lowest-priced) on the market. Here are a few nosotros'd recommend checking out.

The information contained on The Mortgage Reports website is for informational purposes only and is non an advertisement for products offered past Total Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Source: https://themortgagereports.com/13222/10-biggest-benefits-of-a-va-home-loan

Posted by: mayafrefacluste.blogspot.com

0 Response to "Can You Get Larger Home Loan For Repairs Furniture Va Loan"

Post a Comment